As every year in April, the income tax filing season opens in France. Salaries, pensions, amounts to be reported, forms to be completed: the rules applicable to Luxembourg-sourced income rely on a precise reporting mechanism. Taxpayers residing in France who have received income in Luxembourg must declare it using Form 2047, and then transfer it to Form 2042.

This article outlines the essential information and procedures you need to know to complete your tax return 😊

Form 2047, Section 1:

In Form 2047, Section 1 must include:

- The name of the taxpayer;

- The country where the income originates: in this case, Luxembourg;

- The nature of the income (private/public): for information, pensions paid by the CNAP for professional activity carried out in the private sector are considered public pensions (a private pension refers to income not paid by a state institution, but arising from personal initiative or a private contract, such as a third-pillar scheme);

- The amount of income: after deducting only social security contributions.

For salaries, you must not deduct the standard expense allowance of €540 or the Luxembourg tax already paid.

Regarding pensions, you must not deduct the enhanced pension tax credit or the Luxembourg tax already paid.

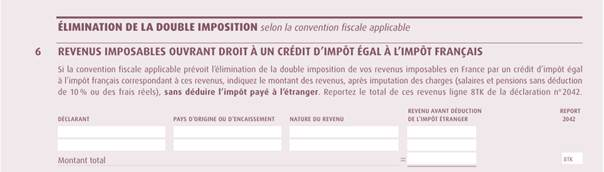

Form 2047, Section 6:

The income must be reported a second time in Section 6 of Form 2047, entitled “taxable income eligible for a tax credit equal to the French tax.”

The amount to be indicated corresponds to Luxembourg income after deduction of social security contributions:

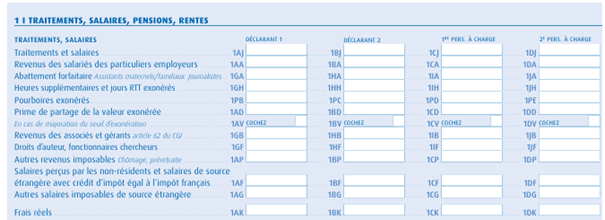

Form 2042, Section 1 – Salaries:

The amounts declared in Form 2047 must then be carried over to Form 2042.

Luxembourg salaries must be reported in boxes 1AF or 1BF, depending on the income recipient.

In the case of remote work and if the 34-day threshold is exceeded, the corresponding amount must be reported in box 1AG or 1BG, depending on the income recipient.

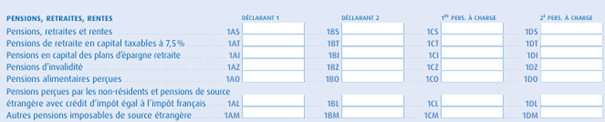

Luxembourg pensions are to be reported in boxes 1AL or 1BL, depending on the beneficiary.

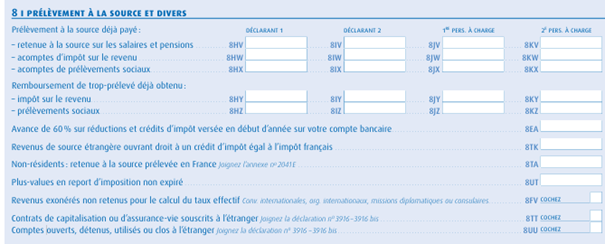

Form 2042 section 8:

The total amount of the relevant income must finally be entered in box 8TK of form 2042. This reporting allows the corresponding tax credit to be applied:

To assist taxpayers with their procedures, several resources may be useful:

The official tax website offers step-by-step guidance for online declarations, with a screen-by-screen breakdown that helps users better understand each stage of data entry: Maquette des démarches en ligne des usagers particuliers

In addition, the tax guide from our partner dedicated to Franco-Luxembourg cross-border workers is available for free download and provides a detailed overview of the main rules applicable to income tax declarations: Guide déclaration fiscale pour les frontaliers franco-luxembourgeois